Data Cloud for Banking: What We’ll Cover

- In this post we will demystify CDP, Salesforce Data Cloud, Salesforce Genie: what’s a buzzword and what’s real; what each can do now plus what's on the roadmap

- Banks and Credit Unions have been on a journey to use their data for some time, but many are still struggling to get data out of backend systems and into a single place

- For those that have got to that first step, the next challenge is actually doing something useful with that data, other than nightly integrations into internal systems

Why You Should Care

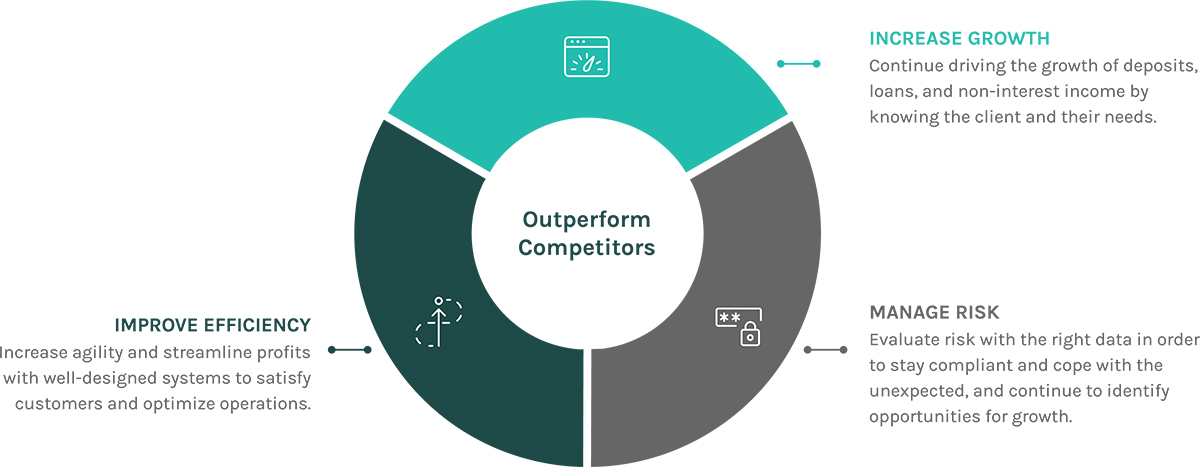

First, it's important to understand why all this matters, and then we can explain how it works and what you should do to improve efficiency, increase growth, and manage risk across your institution.